Let’s be real for a second. When someone tells you to “save more money,” your brain probably does a little eye roll. I get it. Mine used to do the same thing.

For the longest time, I had mates who swore they couldn’t save. There was always something like car repairs, birthday pressies, that thing they absolutely needed from Amazon at 2 AM. And honestly? I’d been there too. Every month felt like this financial treadmill where money came in and immediately disappeared into some void I couldn’t quite explain.

But here’s what I’ve learnt after years of trying (and failing, and trying again): building wealth isn’t about making dramatic sacrifices or suddenly earning twice your salary. It’s not about living on two-minute noodles and cancelling every fun plan you have.

It’s actually way simpler than that. And way less painful.

The real secret is creating small, totally doable habits that make saving feel natural instead of like pulling teeth. It’s about setting up a system where putting money away becomes the path of least resistance, not some heroic act of willpower you have to summon every single day.

This isn’t about turning into someone who reuses tea bags and never buys coffee. It’s about building a life where your money actually works for you, where you’re not constantly stressed about the balance in your account, and where you can actually afford the things that matter to you.

Whether you’re saving for a house deposit, trying to get out of debt, planning a trip that doesn’t involve maxing out a credit card, or just wanting to sleep better at night knowing you’ve got a cushion, these habits will get you there.

So let’s talk about what actually works.ving financial peace isn’t about making massive, painful sacrifices? What if it’s not about earning a six-figure salary or winning the lottery?

The truth is, building a healthy savings account is the result of small, consistent, and often automatic habits. It’s about creating a system where saving money becomes the easy choice, not the difficult one. It’s about shifting your mindset from restriction to empowerment. This isn’t a guide to becoming a miser; it’s a roadmap to building a life where your money works for you, not the other way around.

By transforming your approach and implementing a few key habits, you can build the financial future you dream of—whether that’s a down payment on a house, a debt-free life, a dream vacation, or the simple, profound security of knowing you’re prepared for whatever life throws your way.

Let’s dive into the habits that will get you there.

Part 1: The Foundation – Getting Your Head in the Game

Before we talk about numbers and accounts and apps, we need to talk about mindset. Because trust me, without getting this part right, no savings strategy in the world is going to stick.

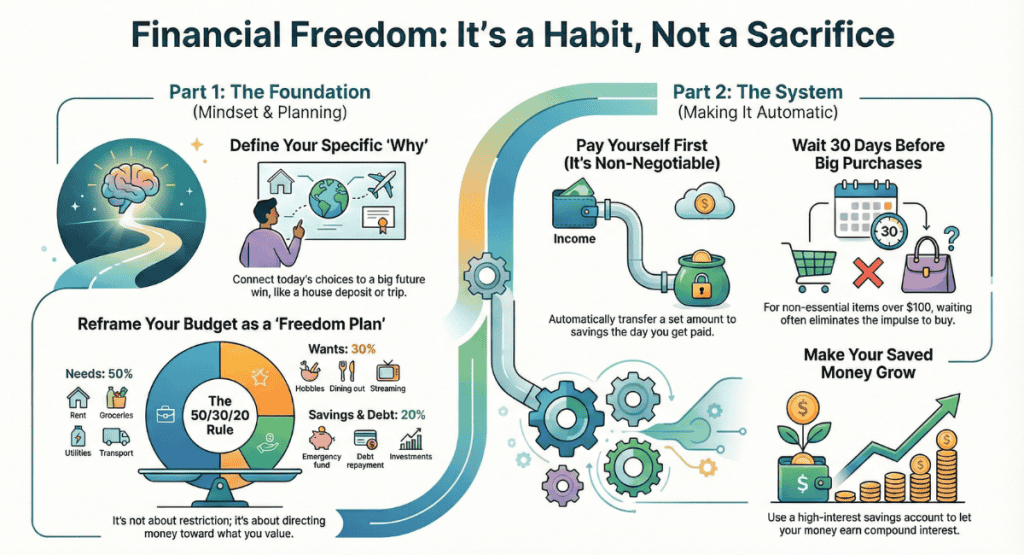

Habit 1: Know Exactly Why You’re Doing This

Saving money just to save money? That’s a fast track to giving up in three weeks. You need a reason that actually matters to you—something that makes you care when you’re staring at a shopping cart full of stuff you don’t need.

Stop saying “I should save more” and start getting specific. Really specific:

- “I’m putting away $10,000 for an emergency fund so I can stop panicking every time my car makes a weird noise.”

- “I’m saving $3,000 for a trip to Italy in two years because life’s too short and I’ve always wanted to see the Amalfi Coast.”

- “I’m building up $25,000 over the next four years so I can finally stop throwing money at rent and buy my own place.”

Write it down. Put it somewhere you’ll see it. Change your phone wallpaper to a picture of your goal if that helps. When you connect today’s small choice to tomorrow’s big win, suddenly skipping that impulse buy doesn’t feel like deprivation—it feels like progress.

Habit 2: Stop Calling It a Budget (Call It Your Freedom Plan)

The word “budget” makes most people want to run screaming. It sounds restrictive and boring and like something a stern accountant would force on you.

So let’s rename it. This is your freedom plan. It’s not about what you can’t have—it’s about directing your money towards the stuff you actually care about.

The 50/30/20 rule has saved my sanity more times than I can count:

- 50% for Needs: Rent, utilities, groceries, transport, insurance – the stuff you actually need to function.

- 30% for Wants: Dinner with mates, streaming services, hobbies, that ridiculously expensive candle that costs $40 but smells amazing.

- 20% for Savings & Debt: This goes straight to your future – emergency fund, super, crushing that credit card debt.

You can use apps like Pocketbook or YNAB, or just a simple spreadsheet if that’s more your speed. The point is to see where your money is actually going, because you can’t fix what you can’t see.

Habit 3: Give Yourself Grace When You Mess Up

You will mess up. You’ll have a shocker of a week and order Uber Eats four nights in a row. You’ll see something online and click “buy” before your rational brain has a chance to intervene. It happens to literally everyone.

The difference between people who succeed at saving and people who don’t isn’t that some people never mess up. It’s that successful savers don’t let one slip-up become a full-blown financial spiral.

This is what I call the “stuff it” effect: “Well, I already blew my budget this week, so stuff it, might as well buy that expensive thing I’ve been eyeing.” Don’t fall into this trap.

Instead, just acknowledge it, learn from it, and move on with your next decision. Consistency over time beats perfection every single time.

Part 2: The System – Making It Automatic (So You Don’t Have to Think)

The best habits are the ones you don’t have to think about. Build a system, and willpower becomes optional.

Habit 4: Pay Yourself First (This Is Non-Negotiable)

This is the habit that changed everything for me. Most people spend their money on bills and life and whatever’s fun that month, and then save whatever’s left over. Which is usually… nothing.

Flip it around. The day your pay hits, have money automatically transfer to your savings account. Whether it’s $50 or $500, make it disappear before you have a chance to spend it.

This isn’t about being noble or having incredible discipline. It’s about removing the decision entirely. You can’t spend what you don’t see.

Habit 5: Let Technology Round Up for You

This one feels like cheating, and I love it. Apps like Raiz and some bank apps will round up your purchases to the nearest dollar and stash the difference in savings or investments.

That $3.50 coffee becomes $4.00, with $0.50 going into your savings. It’s invisible. You won’t even notice it. But over a year, those tiny amounts add up to real money, sometimes hundreds or thousands of dollars and you didn’t have to do anything.

Habit 6: Automate Every Bill You Can

Late fees are the absolute worst. They’re basically a tax on being disorganised, and nobody needs that.

Set up direct debit for everything: rent, utilities, car payments, credit cards (at least the minimum). Not only does this save you from wasting money on late fees, it also protects your credit score and gives you a clear picture of what you actually have left to work with each month.

Part 3: The Daily Tactics – Where the Real Money Is

This is where small changes add up fast. Tiny tweaks to how you spend day-to-day can free up a shocking amount of money.

Habit 7: Wait 30 Days Before Buying Anything Big

Impulse purchases are the enemy of intentional living. To fight back, I use the 30-day rule for anything over $100 (or whatever threshold makes sense for you).

When you want to buy something, write it down. Then wait. At the end of 30 days, look at the list again. Most of the time, the craving will have completely disappeared. And if you still want it? Cool, then buy it knowing it’s a real choice, not just your brain’s dopamine receptors making decisions for you.

Habit 8: Unsubscribe from the Temptation Machine

Those daily emails from your favourite stores aren’t just innocent updates. They’re carefully designed to make you feel like you’re missing out and need to buy RIGHT NOW.

Take 15 minutes and go on an unsubscribe rampage. Email lists, social media accounts from brands that exist only to make you want things—get rid of them. Curate your digital environment so it’s not constantly screaming at you to spend money.

Your wallet will thank you.

Habit 9: Plan Your Meals (Even If You Hate the Idea)

Food is probably one of your biggest expenses, and it’s also one of the most fixable. Spending an hour on Sunday to plan your week’s meals and make a shopping list can save you hundreds every month.

It stops those expensive last-minute takeaway orders and cuts down on food waste (which is literally just throwing money in the bin). You don’t have to become a meal prep influencer—just having a plan makes all the difference.

Habit 10: Think in Cost-Per-Use, Not Just Price

This mindset shift is huge. Instead of always buying the cheapest option, start thinking about how much something costs per use.

A $30 pair of shoes you wear five times? That’s $6 per wear. A $180 pair of quality boots you wear 300 times? That’s $0.60 per wear.

Investing in quality items that last saves you money over time. Plus, you end up with stuff you actually like instead of constantly replacing cheap things that fall apart.

Part 4: Making Your Money Grow

Saving is step one. But you also want that money to actually work for you whilst it sits there.

Habit 11: Get a High-Interest Savings Account

If your savings are sitting in a regular bank account earning basically nothing (like 0.01% interest), you’re leaving money on the table. Online banks and some traditional banks offer high-interest savings accounts with rates that are significantly better.

Your money grows faster just by existing there, thanks to compound interest. Same government guarantee, same safety, way better return. It’s a no-brainer.

Habit 12: Save Your Windfalls Immediately

When you get unexpected money like a bonus, tax refund, birthday cash, money from selling stuff, the temptation is to treat it as free spending money.

Instead, make it a habit to immediately transfer at least half of any windfall straight into savings or towards paying off debt. Think of it as a present to your future self. These windfalls can be massive accelerators for your goals if you let them.

Habit 13: Have a Monthly Money Date

Once a month, sit down for 20 minutes and check in with your finances. Review your budget, see how you’re tracking towards your goals, look for any areas to improve.

This keeps you engaged and aware. You’ll catch problems early, you can make adjustments, and most importantly, you get to celebrate your wins. Seeing that savings number go up is incredibly motivating.

The Bottom Line

You don’t need to implement all 13 of these habits tomorrow. That’s overwhelming and honestly, a great way to burn out and quit.

Just pick one. Maybe it’s automating your savings. Maybe it’s unsubscribing from all those marketing emails. Start there. Get that one habit down until it feels natural. Then add another.

Every single dollar you save is a vote for the future you want. It’s choosing freedom over stress, security over uncertainty, and a life you designed instead of one that just happened to you.

The journey starts with one habit. Just one. Pick it. Start today.

Your future self is going to be so glad you did.